Life doesn’t always line up neatly with open enrollment. When a significant life event occurs, employees may be able to update their benefits outside of open enrollment (known as a midyear election change or qualifying event). Two separate laws govern midyear changes:

- Health Insurance Portability and Accountability Act (HIPAA): Requires group health plans to offer special enrollment opportunities outside of regular enrollment periods in certain situations.

- Internal Revenue Code Section 125: Allows employers the option to design their cafeteria plans to permit midyear changes when the employee experiences a recognized event, the plan allows changes for that event and the change is consistent with the event.

Compliance Tip: A cafeteria plan may be designed to permit midyear election changes that correspond with HIPAA special enrollment events, allowing participants to pay for health coverage on a pre-tax basis. If the plan doesn’t allow such changes, eligible employees must still be allowed to enroll, but premiums will be paid on an after-tax basis.

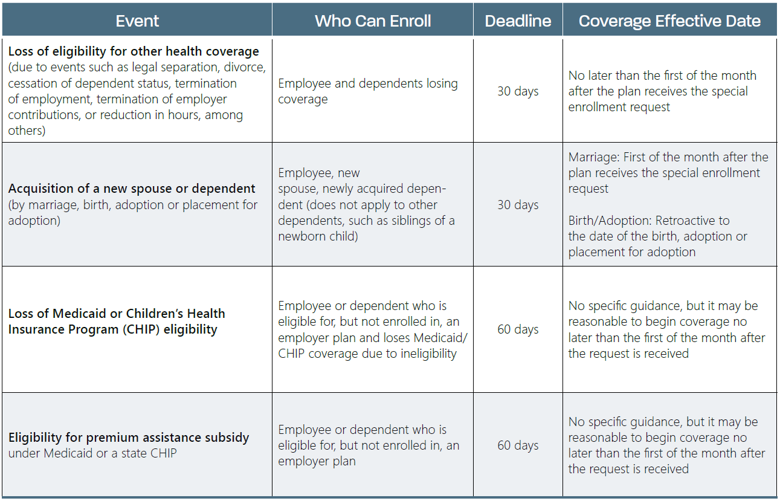

HIPAA Special Enrollment Rights

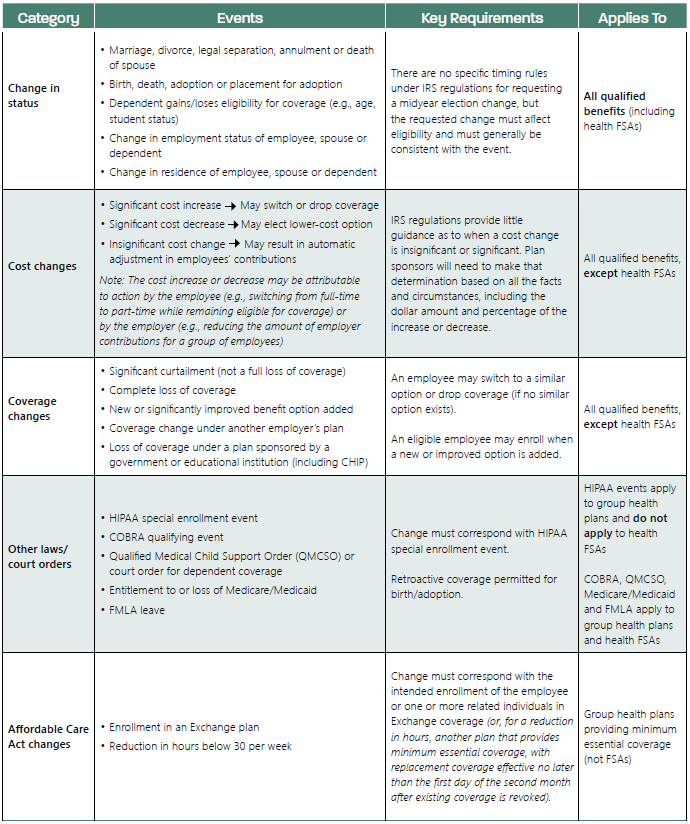

IRS Section 125 Election Changes

Some of the IRS’ midyear election change events apply to all qualified benefits that can be offered under a cafeteria plan. However, other midyear election change events apply only to certain qualified benefits—for example, not all of the IRS’ midyear election change events apply to elections for health flexible spending accounts (FSAs).

Health Savings Account (HSA) Special Rule: Employees may start, stop, increase or decrease their HSA elections at any time during the plan year, as long as the change is effective prospectively. Changes must be permitted at least monthly and upon loss of HSA eligibility.

Key Takeaways

When an employee reports a qualifying event, employers should keep the following in mind when administering midyear changes:

-

Adhere to enrollment deadlines.

HIPAA special enrollment rights are time-sensitive (30 or 60 days from the qualifying event). Employers should apply these deadlines consistently across all employees, as accepting late enrollment requests on a case-by-case basis may create compliance risks.

-

Verify the change is consistent.

Under Section 125, the requested election change must logically correspond with the event, so employers should confirm that the change is consistent with the event before processing it. Changes that do not correspond with the event (for example, dropping coverage after gaining a dependent) should not be permitted. As a best practice, many plan sponsors impose a reasonable deadline (e.g., typically 30 days from the event) in their plan documents to help ensure the consistency requirement is satisfied and to maintain proper plan administration.

-

Ensure the plan document supports the change.

IRS-permitted changes are only available if the cafeteria plan document is designed to allow them. Employers should regularly review their plan documents to confirm that midyear election changes are clearly defined and that day-to-day administrative practices align with plan terms.

-

Apply benefit-specific rules carefully.

Health FSAs are subject to more restrictive midyear change rules than other cafeteria plan benefits. By contrast, HSA contribution elections may be changed at any time on a prospective basis. Employers should apply the correct rules for each benefit type and avoid treating all midyear election change requests the same.

This article is intended as a general reference. For complex situations or plan-specific questions, consult your benefits counsel or plan document. © 2026 Zywave, Inc. All rights reserved.